Patience vs Payoff: What HDFC Bank’s investors can learn from Sachin Tendulkar

Sachin Tendulkar walks out to bat against England in a crucial test match. The whole stadium erupts in almost religious frenzy. “Saaaachinnnn, Sachin…”. The English players look around nervously as over 40,000 spectators chant their idol’s name in rhythmic unison.

Sachin starts gingerly, taking 14 balls to score his first run. As the 19th over began, James Anderson bowled a straight delivery outside the off stump. Sachin played his trademark drive but only managed to clip the ball with the toe end of the bat, offering a simple catch to the wicketkeeper.

A hush descended on the stadium as he started to walk back to the pavilion. And then, the unthinkable happened. A section of the crowd started booing. The ‘Little Master’ was being jeered at in his home stadium! In a cruel irony, even people seated in the Sachin Tendulkar Stand were booing him.

To say that he was having a bad day at the office would be putting it mildly. He was, in fact, in the middle of a horrendous dry spell stretching years. A string of flops, chronic health issues and a deluge of negative press had almost made him hang up his boots.

And yet, his greatest glories lay ahead of him—goes to show how even legends are not immune to incredibly long stretches of doubt and underperformance.

Perhaps no group can appreciate this message more at the current juncture than the investors of HDFC Bank.

Delayed gratification

India’s largest private sector bank had taken the market by surprise two years back when it announced a mega merger with its parent Housing Development Finance Corporation (HDFC) in India’s biggest-ever M&A deal.

The focus was on synergies and cross-selling opportunities. It also touted the potential benefits for the housing sector and the economy as a whole in the form of improved credit flow.

HDFC Bank stock rallied 10% on the day of the announcement (4 April 2022) to close at ₹1,657. The stock is currently trading near ₹1,736, translating into a groan-inducing return of 4.7% in two-and-a-half years.

Why has a marquee blue-chip name like HDFC Bank not budged much in over two years?

Finding a linear ‘cause-and-effect’ relationship in equity markets is often a fool’s errand, but one thing is clear. Mr Market has once again displayed in remorseless fashion its cold and rational side—what may be good for the company or the economy, may not necessarily be good for the stock.

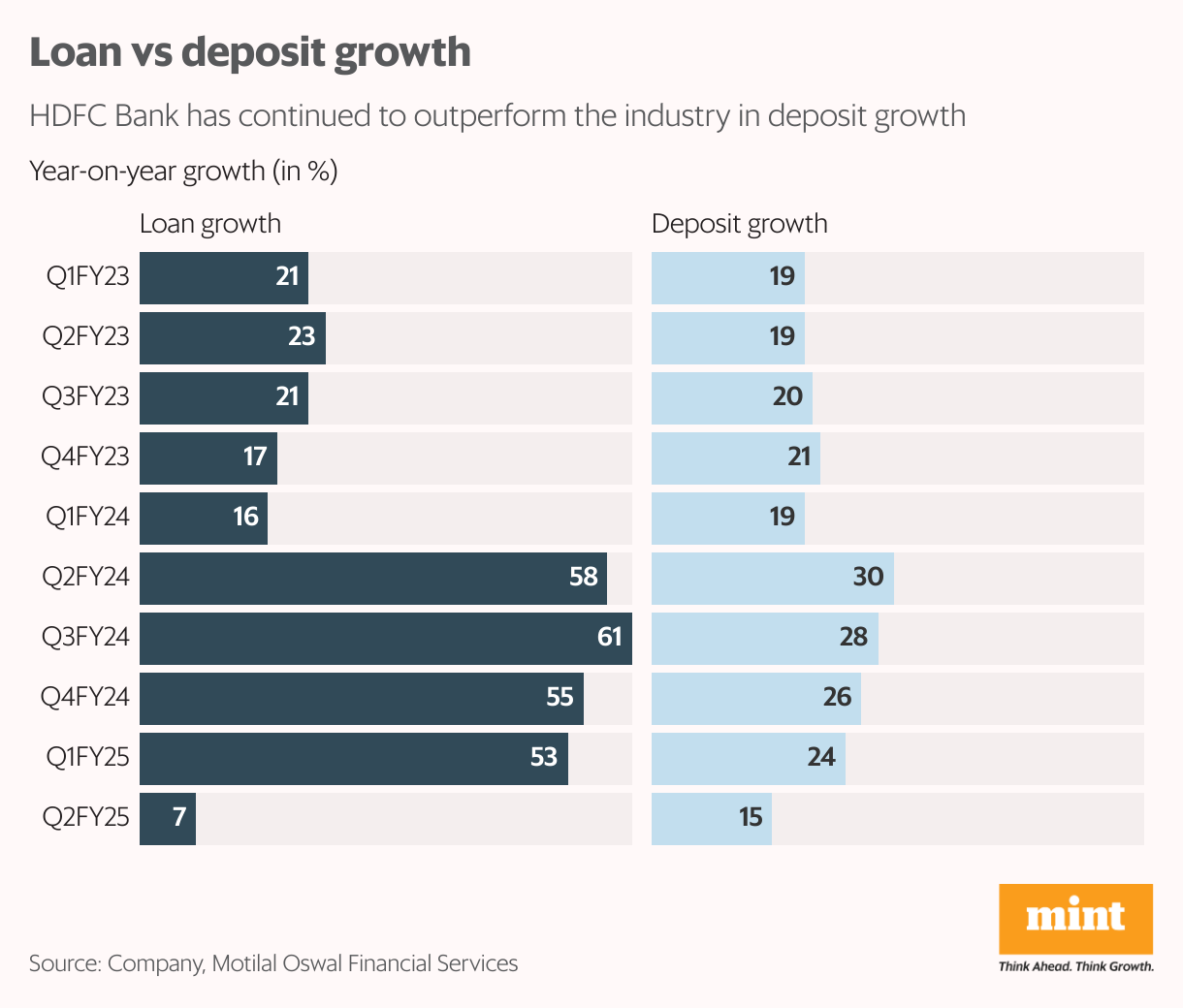

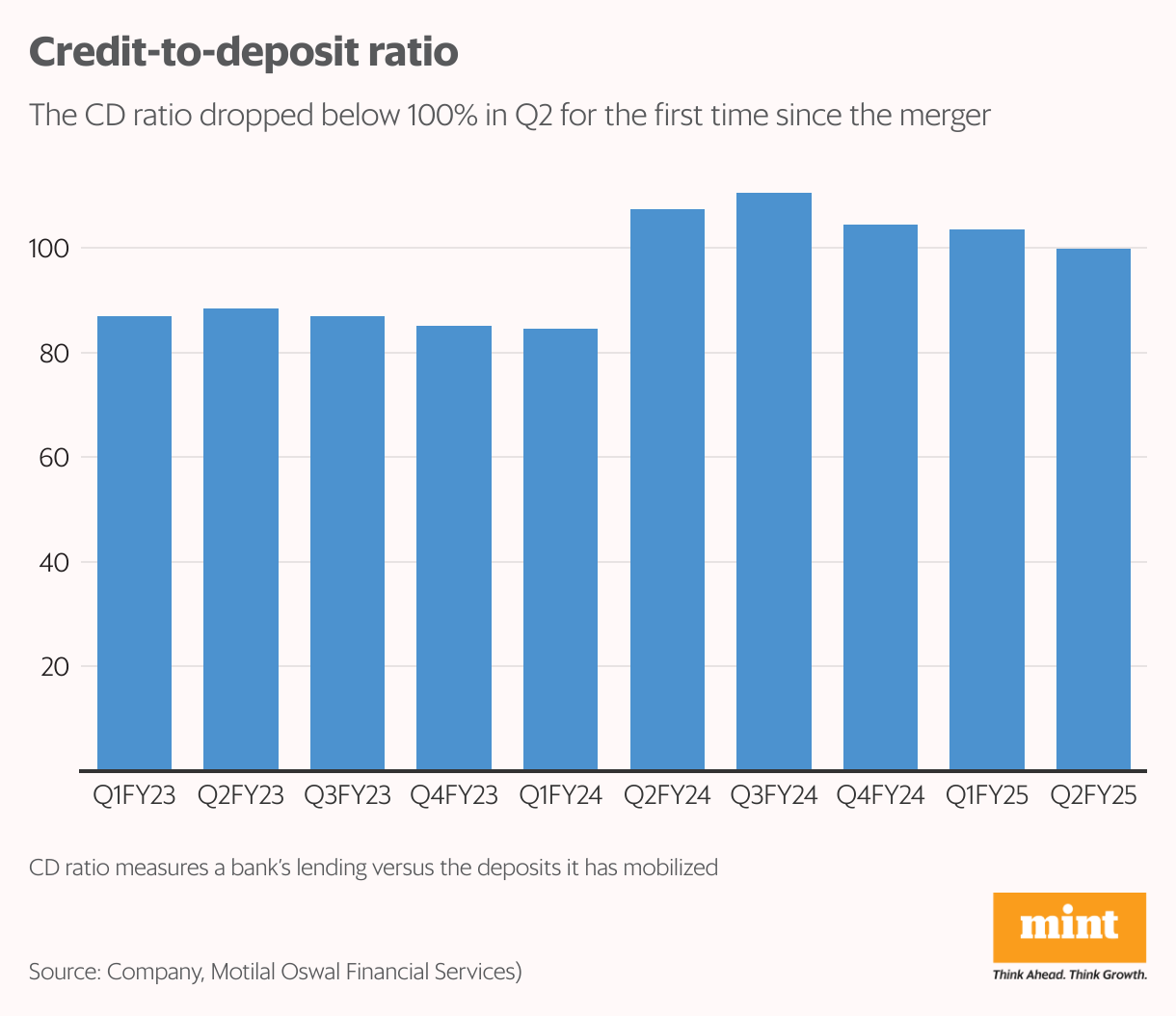

The major concerns of the Street were sustainability of growth momentum on such a large balance sheet, and the merger’s impact on key metrics like net interest margins (NIMs) and loan-to-deposit ratio (LDR). From pre-merger levels of 85-89%, HDFC Bank’s LDR shot up to 110%, before gradually moderating.

The LDR, which compares a bank’s total loans to its total deposits for a given period, is a key tool for assessing the liquidity of a lender. A high LDR means a bank may not have enough liquidity in case of any unforeseen fund requirements.

While the Reserve Bank of India (RBI) does not have any regulatory threshold for LDR, it is understood that the regulator is comfortable with a range of 70-80%.

View Full Image

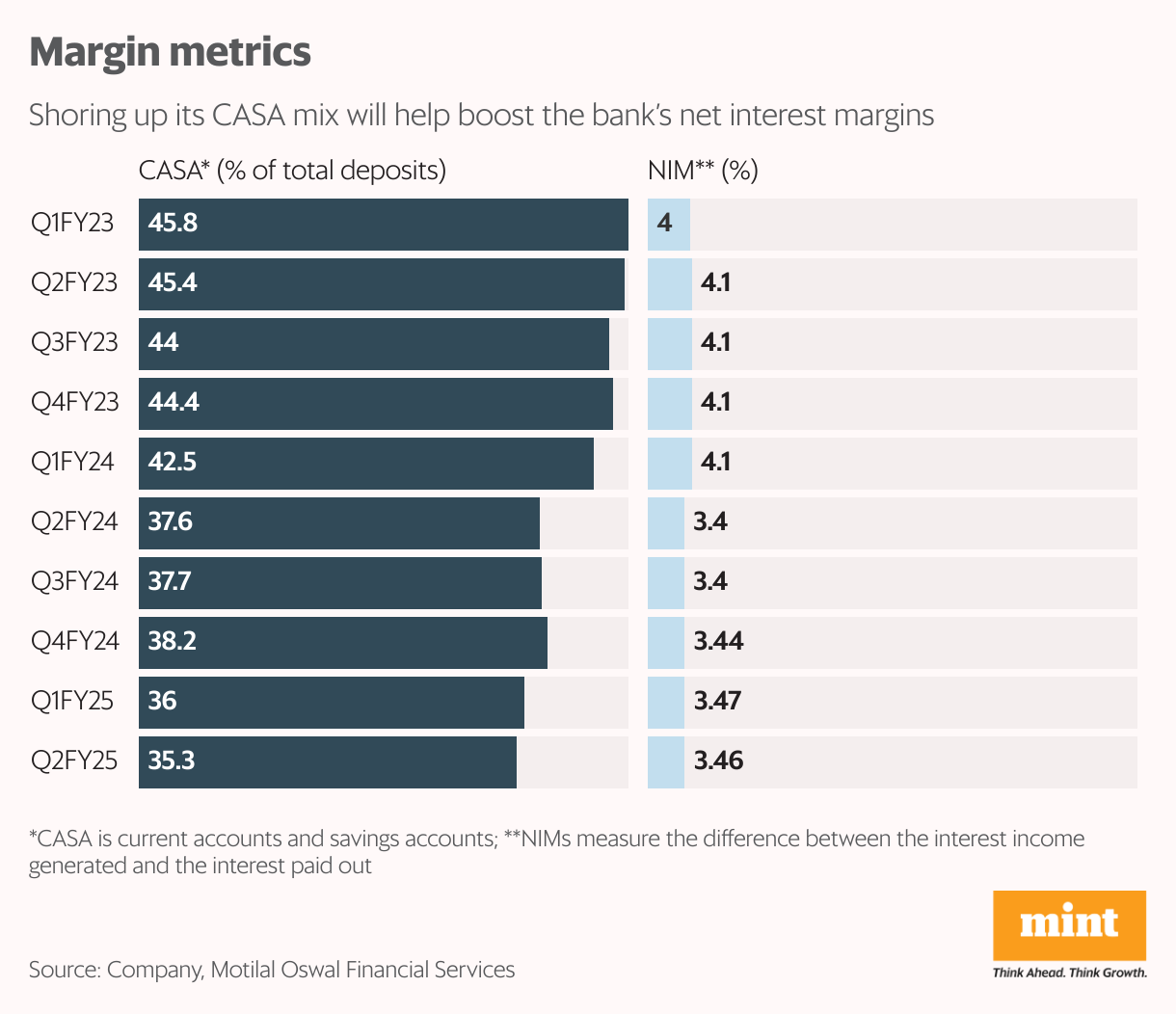

On the margins front, HDFC Bank’s NIMs, which measurethe difference between the interest income generated and the interest paid out, have dropped since the merger as it absorbed HDFC’s huge portfolio of home loans, which offer lower yields compared to other products like auto, personal and SME loans. The bank also had to absorb erstwhile HDFC’s high-cost borrowings, putting further strain on its balance sheet.

For HDFC Bank, the solution to most of its problems lies in deposit mobilization. A healthy growth in deposits would not only bring the LDR under control but also prop up its margins by substituting high-cost borrowings. But as luck would have it, the entire banking sector is facing a severe deposit crunch currently, with a raging bull run in equities inducing investors to junk fixed deposits (FDs) in favour of stocks and mutual funds.

Which is why HDFC Bank’s latest quarterly results have come as a relief for investors.

Q2 show

In the September quarter, HDFC Bank clocked a 5.3% year-on-year rise in net profit at ₹16,821 crore, surpassing the average estimate of ₹16,284 crore in aBloomberg survey of analysts.

More importantly, deposit growth outpaced credit growth by a wide margin. Total deposits grew by more than 15% to cross the ₹25 trillion mark, while gross advances increased by 7% to ₹25.19 trillion.

Consequently, the credit-to-deposit ratio (CD ratio), which measures a bank’s lending versus the deposits it has mobilized, dropped sharply by 375 basis quarter-on-quarter (q-o-q) to stand below 100% for the first time since the merger.

At its post-earnings conference call, HDFC Bank’s chief financial officer Srinivasan Vaidyanathan exuded confidence about reaching the pre-merger levels in two-three years.

“Our CD ratio is presently at 99.8%, previous to the merger we were at 86-87%. The merger’s effect was to take it to 110%…It is in the interest of better economics that we fund the balance sheet with more deposits and less of borrowings,” he said. “Post-merger, our borrowings were at 21% of the total book. Pre-merger, we were at 8% and currently, we are at 16%,” he further addedthat the bank has some distance to go to bring it down—possibly in two-three years.

A key component of the bank’s endeavour to bring down the CD ratio is pruning its loan book by selling chunks of it to various institutional investors. Over the last two quarters, it has securitized loans worth around ₹25,000 crore.

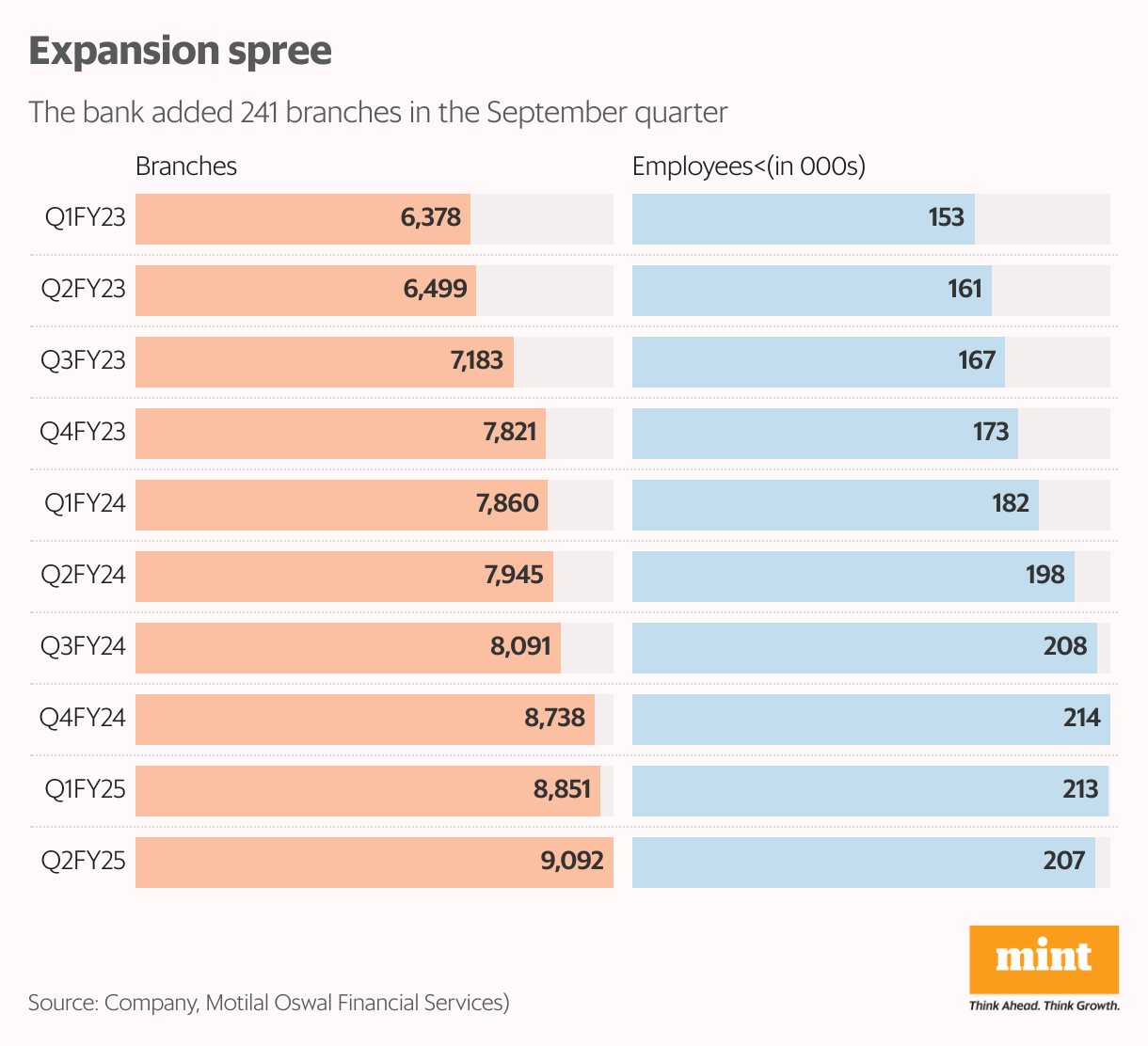

That said, the bank’s number one priority remains deposit mobilization, leveraging its wide branch network. Around 84% of its deposits come from retail branches.

HDFC Bank set up 241 branches during the quarter, taking the total to 9,092 branches across 4,088 cities and towns, serving around 96 million customers. Also, 51% of its branches are in semi-urban and rural areas.

The strength of this relationship was evident in Q2 which saw time deposits growing by a robust 19.3% on-year to ₹16.16 trillion. However, current accounts and savings accounts (or CASA, which are a low-cost source of funds for banks) growth stood at 8.1%.

“The CASA ratio saw a q-o-q dip to ~35% as time deposits growth accelerated, but the trend (is expected) to normalize with rural CASA set to improve over the mid- to long-term. The ageing of branches will lead to healthy deposit growth led by sticky and granular rural/urban FD and CASA flows,” InCred Equities said in a note dated 20 October.

On the advances front, HDFC Bank has increased its focus on unsecured retail lending (other than mortgages), which has grown by 3.8% sequentially, whereas mortgages grew by around 1.9%. Commercial and rural banking also remain important focus areas, growing 4.7% quarter-on-quarter. All these segments are expected to support overall yields in the mid- to long-term.

The NIM was flat sequentially at 3.65% (based on interest earning assets), which is a further testimony to the bank’s stance on chasing profitable growth and not getting into a rate war.

“HDFC Bank is our high-conviction ADD-rated stock with a stable target price of ₹2,150, as we continue to believe that the bank’s transition phase is on track. We expect it to be ~2% RoA (return on assets) and ~16% RoE (return on equity) story,” InCred equities added.

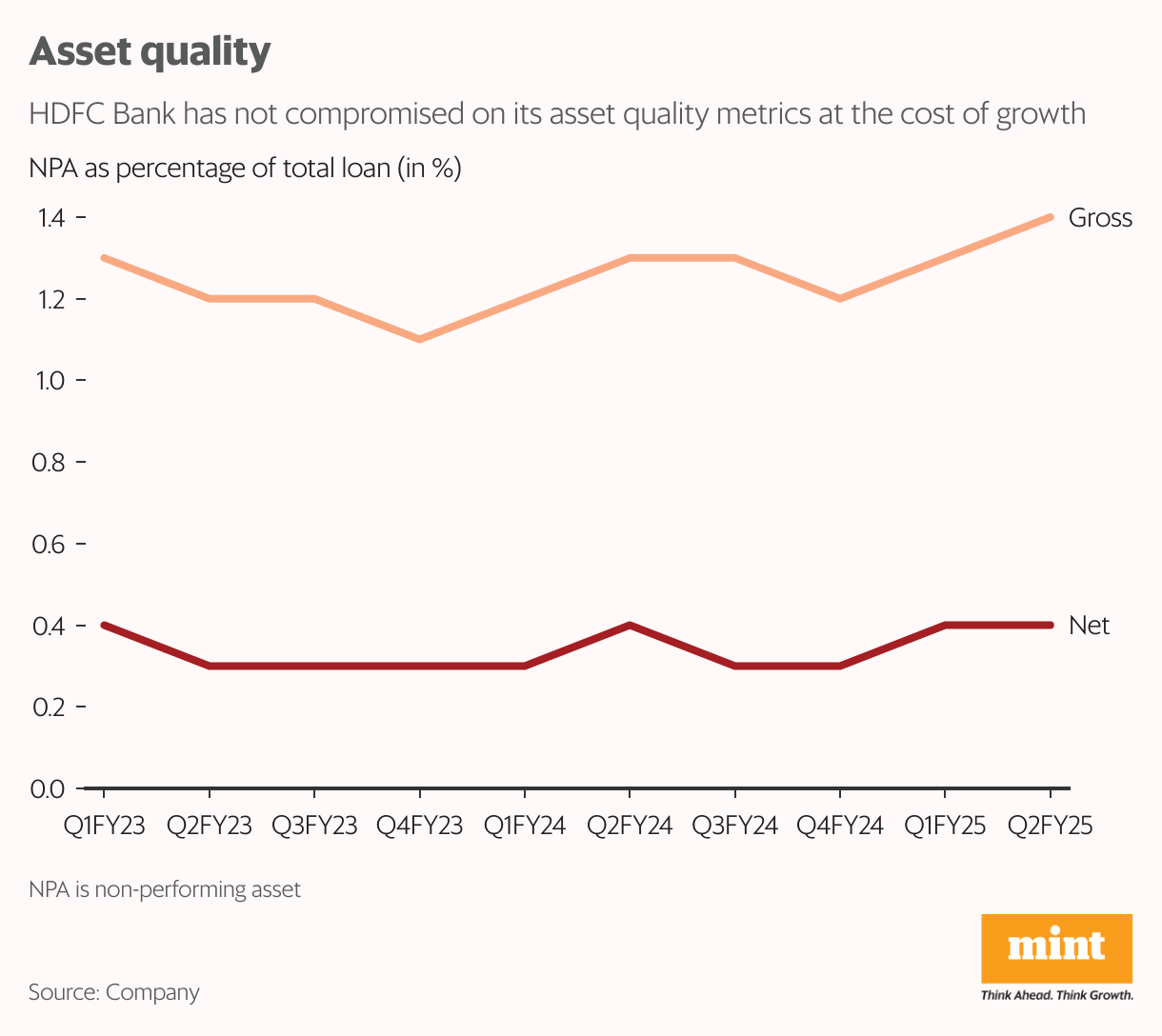

The bank reported a slight dip in asset quality metrics in the second quarter. The gross non-performing asset (NPA) ratio worsened to 1.36% from 1.34% a year ago, while net NPA ratio stood at 0.41% as against 0.35% earlier.

Worst over?

Despite the slight uptick in NPAs,analysts remain positive about the lender’s asset quality.

“HDFC Bank has been able to maintain pristine asset quality across cycles and this can be credited to its strong underwriting practices and risk-calibrated lending. Currently, amid stress in the unsecured portfolios at a systemic level, HDFC Bank’s unsecured portfolio continues to perform well, with retail GNPA at 0.8%,” Axis Securities said in a note to clients.

“This is primarily owing to the bank being ahead of the curve in identifying stress based on early warning indicators and pruning growth in the unsecured segment. Asset quality in the other segments (commercial and rural banking, agri and corporate) continues to remain healthy, given the bank’s ability to judiciously balance between growth and risk,” the note added.

It has a ‘buy’ rating on the stock with a target price of ₹2,025, implying a potential upside of around 17% from the current levels.

Does this mean the worst is over for the bank?

“I think we should wait for another quarter and look at the metrics, but yes, it does seem to have bottomed out. HDFC Bank has been the only private bank stock which has not seen any price action for the past two years, so this also presents the perfect opportunity for investors to accumulate the stock,” Rajesh Palviya, senior vice president of research (head, technical and derivatives), Axis Securities, told Mint.

“We should also remember that this name is a favourite of FIIs (foreign institutional investors). So, once they start increasing allocation to the Indian banking sector, HDFC Bank is likely to benefit in a significant way,” he added.

Sum of parts

HDFC Bank was the top gainer in the Sensex pack on 21 October—the first trading day after the results were announced—even as the benchmark closed in the red.

But more than its encouraging Q2 numbers, market experts attributed it to an even more powerful driver—unlocking the value of its subsidiaries.

The HDFC Bank board on 19 October approved selling ₹10,000 crore worth of shares in its subsidiary HDB Financial Services through an offer-for-sale (OFS). Another ₹2,500 crore of fresh shares will be issued as part of the IPO.

HDFC Bank currently owns 94.6% stake in HDB Financial Services, which is a non-banking financial company (NBFC) that provides lending and business process outsourcing (BPO) services to individuals and businesses. HDB Financial Services posted net revenue of ₹24,100 crore during the quarter, with a profit after tax (PAT) of ₹590 crore.

Size does matter

The bank’s performance metrics are improving, deposit growth is among the highest in the industry, subsidiaries are performing well, analysts’ view is unanimously positive (39 ‘buy’, 9 ‘hold’ and 0 ‘sell’ calls as of 22 October), but for the lakhs of HDFC Bank shareholders, there’s only one question on their minds—why is the stock not rallying?

View Full Image

The answer, as it turns out, encompasses an important lesson.

Legendary investor Peter Lynch, in his bestselling book One Up on Wall Street, highlights a fundamental rule of equities, one that is often ignored by participants—big companies do not generally have big stock moves. Citing the example of American conglomerate General Electric (GE), he said it is mathematically impossible for the company to double or triple in size in the foreseeable future.

At the time of writing in 1989, GE represented nearly 1% of the entire US gross national product. Every time an American consumer spent a dollar, nearly a penny went to goods or services provided by GE, like light bulbs, appliances, insurance etc.

“Here is a company that has done everything right—made sensible acquisitions; cut costs; developed successful new products; rid itself of bumbling subsidiaries; avoided getting suckered into the computer business (after selling its mistake to Honeywell)—and still the stock inches along. That’s not GE’s fault. The stock can’t help but inch along since it’s attached to such a huge enterprise,” Lynch pointed out.

Indian investors would do well to keep an eye on HDFC Bank’s size while fantasizing about the stock’s future returns. With a market capitalization of ₹12.97 trillion, it is not only the biggest domestic bank but also the third largest Indian company overall after Reliance Industries ( ₹18.35 trillion) and TCS ( ₹14.85 trillion).

Growing its humongous ₹36.8 trillion balance sheet would take a Herculean effort, not to mention multiple market cycles, during which time at least half a dozen mid-cap lenders or small finance banks would undoubtedly have graduated to the big league.

Stocks, like people, are not immune to life cycles. The early high-growth phase is not likely to recur once a company reaches a certain size.

“The problem with this stock is investor expectations. They see other stocks soaring in this bull run and expect a large cap like HDFC Bank to do the same. It is not going to happen. Even after the bank sorts out its merger-related issues, the stock is not likely to see explosive growth, which is how most mature companies behave. In fact, investors should treat HDFC Bank stock like a tax-efficient form of a high-yield fixed deposit. It is a steady compounder and not a short-term multi-bagger,” a Mumbai-based fund manager, who didn’t want to be identified, said.

Stocks, like people, are not immune to life cycles. The early high-growth phase is not likely to recur once a company reaches a certain size. As cricket fans know too well, even a champion like Sachin Tendulkar, who started out as a swashbuckling youngster, evolved to be a stable run-getter in the second half of his career before he could assume his position in the pantheon of legends.